by Dana Samuelson – American Gold Exchange

The most significant development in the gold market over the past two months has been the unprecedented rally in the dollar. The U.S. currency recently closed its strongest quarter in six years by gaining for a record-breaking eleven straight weeks. Since our last update, in early August, the ICE dollar index has risen 6.7% against a basket of major foreign currencies—an enormous short-term gain, especially for a currency that had been almost flat for a year. Seldom does any market rise so far and so fast without a meaningful correction, and we have yet to see one in this extraordinary run by the dollar.

A rising dollar pressures precious metals and other commodities that are denominated in it for international trade by making them more expensive to users of other currencies. The Bloomberg commodity index has tumbled 8% since early August. Silver has lost 18%, platinum 18%, and palladium 15% during this period. Gold has actually fared relatively well, dropping only 7%—a big fall, yes, but one showing remarkable resilience in light of the dollar’s nearly identical rise.

A rising dollar pressures precious metals and other commodities that are denominated in it for international trade by making them more expensive to users of other currencies. The Bloomberg commodity index has tumbled 8% since early August. Silver has lost 18%, platinum 18%, and palladium 15% during this period. Gold has actually fared relatively well, dropping only 7%—a big fall, yes, but one showing remarkable resilience in light of the dollar’s nearly identical rise.

Because gold trades as a safe-haven currency as well as a commodity, its drop was cushioned by rising geopolitical instability, especially in the Middle East and Ukraine, as well as by the generally slowing economic recovery outside of the U.S. We think this safe-haven role is likely to become more prominent in coming months as the war against ISIS heats up, the conflict between Russia and the Ukraine, currently in a lull but still unresolved, becomes active again, and major economies soften further. Nonetheless, dollar-strength is calling the tune right now.

Why is the dollar so strong? The answer is twofold: relative health in the U.S. economy compared to its weakening peers; and speculation that the Federal Reserve will begin to raise interest rates sooner than mid-2015. These two drivers go hand-in-hand, and we’ll discuss each in turn.

Relatively stronger U.S. growth

While most major world economies are flat or contracting, the U.S. economy is expanding—if only, as the Fed says, at a moderate pace. U.S. GDP year-on-year is up 2.6%. By contrast, the Eurozone’s growth is a meek 0.70% and Japan’s is negative 0.10%. China’s official growth target has dropped to 7.3% from 7.5%, a significant admission of weakness from a nontransparent government that prides itself on being an economic juggernaut. Seldom is there so large a growth-gap between the U.S and other developed world economies as today.

The consequences of this differential are easy to understand when you look at these economies as pieces of the global pie. The U.S. makes up 22.75% of the world economy, the Eurozone makes up 23.50% and Japan 6.75%. With the latter two stagnating, more than 30% of the world is facing a growth-differential with the U.S of nearly 2%—a gap that didn’t exist just six months ago, when the U.S. contracted 2.1% in the first quarter. Factor in China, with 12.5% of the world’s economy, entering its own slowdown, and at least 42.75% of the world is losing momentum while the U.S. is gaining. No wonder global capital is flowing here, boosting the dollar and pressuring commodities.

Since 2008, when the global financial system nearly collapsed and the Great Recession began, central banks have been racing to devalue their currencies through loose monetary policies in hopes of stimulating spending, growth, and employment. After exploding its balance sheet to more than $4.5 trillion, the Fed is scheduled to end the money-printing operation known as quantitative easing but has no plans to drain off this excess liquidity any time soon. Japan and the Eurozone are slated to expand their monetary stimulus in coming months. China, too plans to increase broad-based stimulus, pushing another $80 billion in liquidity into its banking system to combat slower growth.

The world’s tsunami of cheap cash will continue to swell, even if it swells with relatively more euros, yen, and yuan, breeding the risk of higher inflation. In the short term, this divergence in monetary policy between the U.S. and the other major economies may pressure gold by strengthening the dollar. In the longer term, however, the rising inflation-risk engendered by so much global easing should be very bullish for gold.

Interest rates and the Fed

The other primary driver in the dollar’s recent rally has been speculation about when the Fed will begin to raise interest rates from near zero, where they’ve been stuck for six years. Momentum became turbo-charged in mid-September after the Fed raised its median estimate for the federal funds rate from 1.125% to 1.375% by the end of 2015, implying a steeper rise once increases eventually begin. Importantly, the Fed’s policy statement also maintained its stance that interest rates will stay near zero for a “considerable time” after quantitative easing concludes this month, something most analysts took to mean no rate increases until June 2015 at the earliest.

Nonetheless, the Fed’s higher rate projection for year-end 2015 caused forex traders to flood into the dollar from other currencies, especially the euro and yen, which are subject to further devaluation as Japan and Europe struggle for growth. If the global devaluation of currencies is the dirty laundry of the financial crisis, the dollar is looking like the cleanest dirty shirt in the hamper. The question is, for how long.

In the era of globalization even the largest economy cannot succeed in isolation. Without thriving markets in Asia and Europe, demand for U.S. goods and services can only grow so much. The rapid rise of the dollar, therefore, has the potential to undercut the U.S. recovery by making exports uncompetitive. In addition, ever-cheapening imports can curb domestic demand for U.S. goods and create additional deflationary pressures, a serious concern to the Fed.

After all, one of the goals of the unprecedented monetary stimulus of the past six years has been to combat deflation by increasing inflation, which has yet to approach the Fed’s target of 2%. According to Bloomberg, the bond market expects inflation to average 1.61% over the next five years, down from 2% at the start of August, based on differences in yields on government inflation-indexed bonds and U.S. Treasuries of similar maturity.

Indeed, recent speeches by prominent members of the FOMC are beginning to signal concern about dollar’s effect on the recovery. William Dudley of the New York Fed said its rapid rise may work against the goals of boosting employment and combatting deflation by making U.S. exports expensive and imports too inexpensive. Atlanta Fed President Dennis Lockhart added that dollar-appreciation exacerbates the weak domestic and international demand that already hamper the recovery, and may justify delaying any rate increases.

A more dovish shift?

A guiding principle of the Fed under Chair Janet Yellen has been that it’s worse to raise interest rates prematurely and risk damaging the recovery, than to wait too long and risk faster-than-desired inflation. Yellen has said explicitly that she would be willing to push unemployment below its so-called natural rate as she considers the timing for rate increases. Dudley said last week that inflation needs “to run a little hot,” meaning above the Fed’s 2% target, before any monetary tightening.

Other Fed members have also cautioned against raising rates prematurely. Charles Evans of the Chicago Fed advocates being “exceptionally patient in adjusting the stance of U.S. monetary policy—even to the point of allowing a modest overshooting of our inflation target to appropriately balance the risks to our policy objectives.” Minneapolis’ Narayana Kocherlakota warns that rates shouldn’t change before the Fed is certain the economy can withstand higher borrowing costs, and that might take longer than expected.

Meanwhile, the two most hawkish members of the FOMC will depart early next year, giving even freer rein to the Yellen camp. Philadelphia’s Charles Plosser will retire in March and Richard Fisher of the Dallas Fed will step down in April, both in advance of the first likely rate increase. Fisher and Plosser have been the strongest and most consistent dissenters from easy-money policies, arguing vociferously against anything (like quantitative easing or near-zero interest rates) that could spur inflation. With their voices out of the mix, an increasingly dovish Fed may feel empowered to delay rate-increases for longer than many now think.

With the U.S. housing recovery showing signs of stalling, wage-growth stagnant, consumer spending and consumer confidence both depressed, and growth in U.S. manufacturing fluctuating, not to mention global weakness and political shocks in the Ukraine and Middle East, interest rates could easily remain unchanged until 2016. As this possibility filters through forex markets, the momentum of this stunning rally in the dollar could quickly reverse, giving gold and other commodities ample opportunity for a strong rebound.

18-month charts

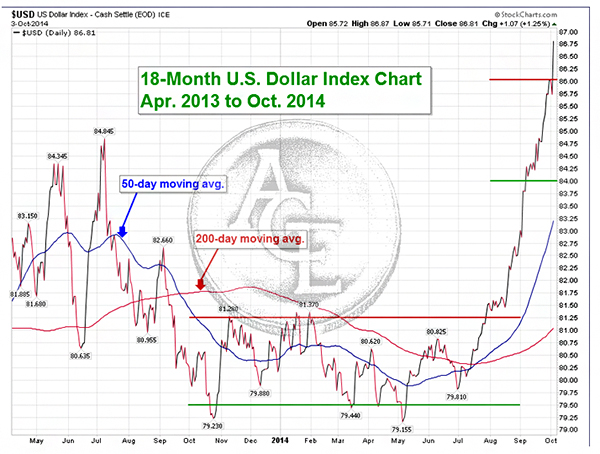

U.S. Dollar

As you can see in the Dollar Index chart above, after tentatively breaking resistance at 81.25 in late July and consolidating at 81.50 for the first half of August, the dollar has gone absolutely parabolic. Throughout August and September the news from Europe and Japan was about economic decline, further monetary easing, and lower interest rates. In the U.S., conversely, the news was about economic improvement (albeit uneven), the end of quantitative easing, and possibly rising rates. The divergence was stark, and it played out in the currencies.

Technically, the dollar was hitting upside resistance at 86 until the U.S. non-farm payrolls report came in stronger than expected last Friday. The buck quickly surged by another 1%, breaking resistance at 86 with an eye toward resistance at 88.40 and 89.1, its 2009 highs.

The dollar’s rise has been unprecedented, as we detailed above, with a record eleven consecutive weeks of gains. And given its momentum, this rally may attract additional inflows before it has run its course. Ultimately, though, whether from profit-taking, speculative exhaustion, or new data that calls into question the comparative strength of the U.S. recovery, it will stall. When that happens, we expect support to consolidate at 84 on the index chart.

Gold

Given the dollar’s extraordinary run, gold has shown more resilience than almost anyone expected. Through August it held support at $1,280. Once the dollar broke sharply higher in early September, gold began to erode in a series of 1% declines until it found major psychological support just over $1,200. This support held until last Friday, when the dollar surged 1% on the strong September payrolls report, pushing gold to $1,190.

Gold is now down about 7% since early August, nearly mirroring the dollar’s 6.7% rise. Notably, the yellow metal has held up much better than the gray ones, with silver tumbling 18%, platinum 18%, and palladium 15%. As we said above, more so than the other precious metals, gold trades as a currency as well as a commodity. Its added role as global safe-haven currency has lent it support and will continue to do so.

In the short term, we expect gold to maintain its typically negative correlation to the dollar—barring some sort of “black swan” crisis that drives gold and the dollar higher together on flights to safety. A test of 2013 major support at $1,180 is still possible. Below that level, we see deeper support at $1,150 and $1,100. However, we doubt the world would let gold become that inexpensive—there’s just too much economic and geopolitical uncertainty afoot. Upside resistance will be found at $1,230 and again at $1,280.

Silver

Silver has been very weak during the past two months, falling 18% from $20 to $16.80 since the start of August. After breaking major support at $18.75, its declines have come in large increments of 50 to 75 cents, punctuated by short periods of consolidation.

More commodity than safe-haven currency, at least compared to gold, silver could fall further if the dollar continues to rally, perhaps to as low as $16 before finding major support. However, we think it will resist more of the big price-drops as bargain-hunters buy aggressively on new dips. With perhaps another $0.75 of potential downside risk, silver looks to have good support at $16.50.

Expect more choppiness in the coming weeks but keep in mind that silver can rally very sharply, and a short-covering rally is overdue. Recent price-drops have been less about fundamentals than momentum, and that can change quickly.

Platinum

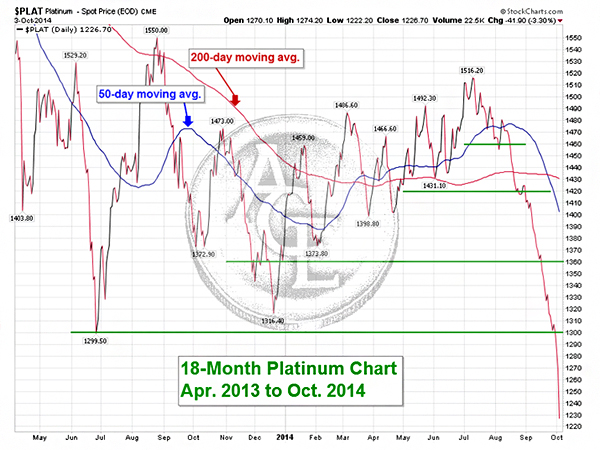

Like silver, platinum has fallen very sharply. After breaking short-term support at $1,460 in mid-August, it held briefly at $1,420 before tumbling to major support at $1,300, held again, and then plunged to $1,225. The market has apparently forgotten about platinum’s projected supply deficit of more than million ounces this year. It’s all about momentum and sentiment at the moment.

Like silver, platinum has fallen very sharply. After breaking short-term support at $1,460 in mid-August, it held briefly at $1,420 before tumbling to major support at $1,300, held again, and then plunged to $1,225. The market has apparently forgotten about platinum’s projected supply deficit of more than million ounces this year. It’s all about momentum and sentiment at the moment.

Platinum should now find support at $1,200 and again at $1,150. Upside resistance will be found at $1,275. As with silver, expect a choppy market in coming weeks.

Palladium

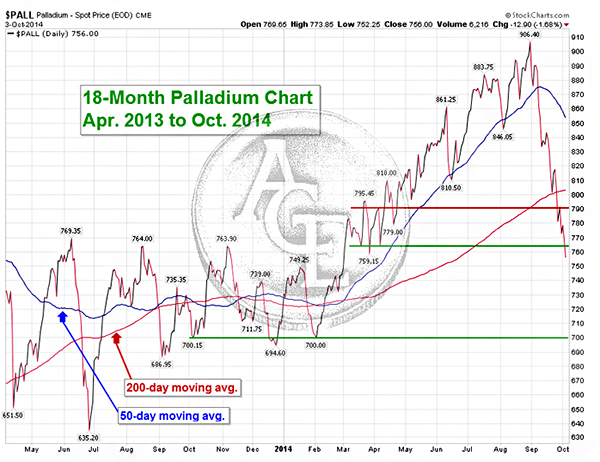

Palladium was trading at $870 on August 1, and initially resisted the dollar’s surge, gaining $36 to reach new short-term high above $906 in late August. Swept up in the commodities sell-off in September, however, it tumbled first to major support at $765, which had held since March, and then to $752 last Friday. Palladium is now down a net 15% since the dollar rally began. Below $765, its next major support level is $700; upside resistance is at $790.

With strong fundamentals, including a projected supply deficit of 1.6 million ounces in 2014, palladium’s correction may have about run its course. According to Johnson Matthey, automobile catalytic converters account for 38% of platinum demand and 68% of palladium demand, worldwide. Rick Rule, an expert investor in natural resources and a founder of Sprott Global, told us in a private conversation last month that China currently has catalytic controls on only around 10% of its cars. Because of its severe problems with air pollution, China plans to increase to 50% in five years and 100% in seven years. China sold as many cars last year as the U.S., so that would mean a huge increase in demand for platinum and palladium.

While the potential for rising Chinese use may be extremely bullish for PMGs in the long run, the current economic slowdown in China and in Europe is still likely to hamper demand in the near term. Once the current route in commodities is over, and it might be over soon, we’ll look to buy PMGs aggressively to take advantage of recent overselling.